I don’t save well. I actually don’t save. A friend helps me with it.

It’s partly because of who I am, and also because I am in jua kali.

You know the process. No next cheque is promised, even if the work was done months ago and the Finance guy has been on leave ever since. Or one signature is missing, and the owner of the hand is in a place with no network.

That process goes something like this. You get the cheque, it is more money than you have ever had at a go. Before you bank it, you have a conversation with yourself. You will not overspend. You will pay your bills, buy something nice for yourself then divide what’s left between your needs and what you want to save. You swear to yourself that when the check matures in two days, the first thing you will do is move ten percent of it to your savings account. Tithing to yourself, you call it. You chuckle, it’s a brilliant plan.

The notification comes just a day in when you are seated in a bar having a beer and taking a break. You facepalm because that motivational talk you were giving yourself now seems like a far off, impossible plan. You pay your bills through the phone and watch as that pie chart goes red as the landlady, the cleaning lady, and that buddy who lent you money take more than half of it. Then the insurance guy, then smaller bills like water and electricity. And none of them seem to allow you to prepay for the dry spell that follows.

By the time you are done seeing just how much you’ve paid, you need another beer, and another. And then a distraction, and then you are getting home at sunrise with a bigger hole where the one you made last night used to be. “Can I survive on what’s left until you get more money?” You ask yourself as the hangover wears off. Can you still afford to pay the ten percent to yourself? What if you move it to the next check, consider it a self-loan. You will even cull 25 percent to punish yourself for not seeing how stupid your last plan was. It’s mid-morning when you pour yourself tea and drag yourself to the table to work for the day. As the dog snuggles herself on your feet, and the tea burns your tongue as the laptop powers on, you smile. It’s a brilliant plan. It will never work. At least not like that.

For some, it’s easier to set a specific target, like the konda who saves 300 bob every day, whether business is good or bad. For others, it’s saving a pre-set portion of each payment, like in my original failed plan. It turns out tithing to a deity is easier than tithing to yourself. Some try chamas, others invest in assets. There is a “to each his/her own” theme in this paragraph, but the underlying moral, if there is one, is that you need to understand your weaknesses in saving, to save. If you are an impulse buyer, find ways to make Loop solve the problem for you. If you are a miser, refer to preceding line.

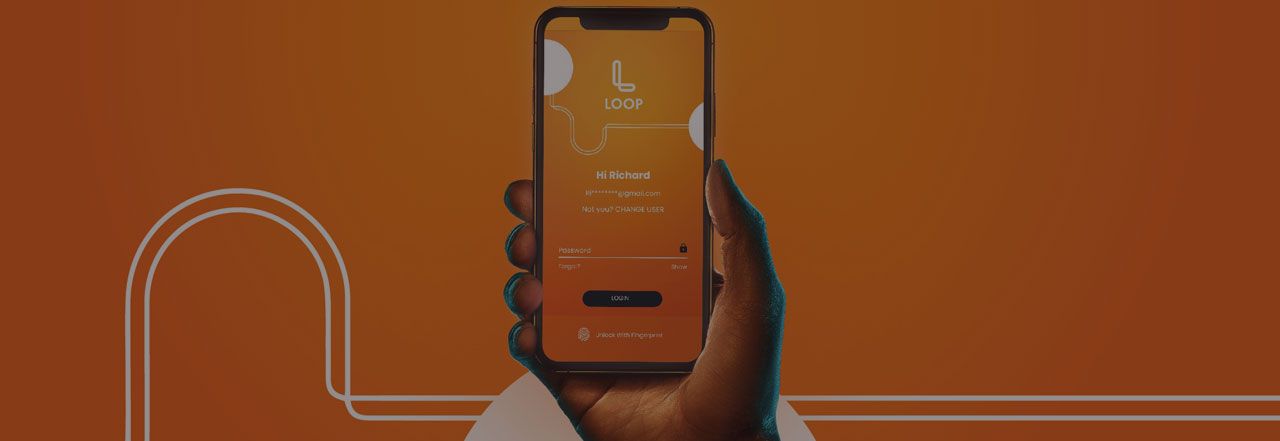

Our relationship with money is complex, especially as everything is getting more expensive while jobs are declining. Add to that that now you can check your banking app at 3 a.m, only to realise the expensive date you promised won’t work. So now you have a reason to work harder tomorrow. Then you search for the car of your dreams and add it to Loop, and now the app won’t stop reminding you of that goal.

I know this wealthy guy who, although he doesn’t need bank loans, is always paying for at least three. He can pay for all of them without hurting his savings, but he says paying for loans is the only reason why he still drives himself to wake every day. I don’t get it, and I doubt I ever will, but the underlying lesson was that if you have everything, you need to create little motivations to save for yourself, and for those you love.

It took me years to realize that although saving seems to come easy to some people, I am not one of them. It’s a habit we have to teach ourselves if it doesn’t come naturally to us. It is asking for help, sometimes from people, sometimes from deities, and often from modern personal banking tools like Loop. Otherwise, I am that guy buying the book on impulse buying without a second thought!

By Owaah